.png?width=200&height=78&name=CH%20Diligence%20(thicker%20line).png "Castle Hall Diligence - Logo.png")

.jpg)

Yesterday, the SEC announced charges against three executives of Premium Point, a well known mortgage backed security / structured credit manager, alleging pervasive valuation fraud. The SEC charged Premium Point’s CEO and chief investment officer Anilesh Ahuja as well as Amin Majidi, a former partner and portfolio manager at the firm, and former trader Jeremy Shor.

The detailed SEC complaint (available here) outlines two issues:

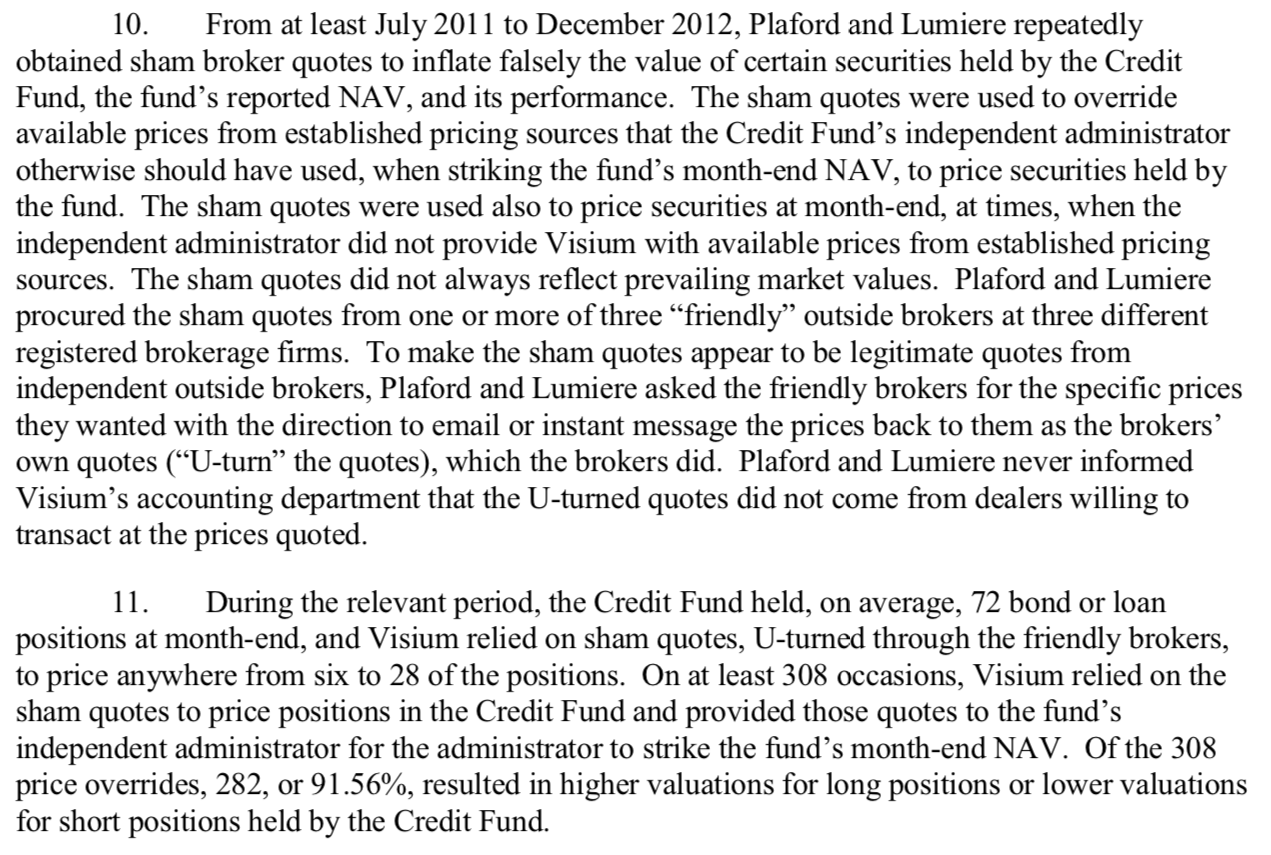

What is particularly interesting is to compare this case to that of Visium, where we have the same broker quote collusion (see SEC complaint). Equally the administrator was prepared to accept "over-ride" prices on several hundred occasions:

Illiquidity and Complexity

Castle Hall continues to see wide variation in valuation practices across the industry, particularly with respect to hard to value securities. Valuation issues arise, of course, either due to illiquidity (thinly traded assets with no depth of market and consequently no reliable external pricing indicator) or complexity. Indeed, we are often more concerned by valuation issues in Level 2 "mark to model" derivatives as compared to "unobservable" Level 3 assets.

Who is Responsible for Pricing?

Ultimately, the core of the pricing dilemma is responsibility. On the one hand, many market participants believe that it is the investment manager's portfolio; the manager knows the instruments best and can therefore lead the pricing process to generate the most accurate prices; and, therefore, the manager should be responsible for pricing. Or - the manager is conflicted and the sorry history of litigation shows far too many examples where managers have fraudulently manipulated pricing (we have yet to see a portfolio manager who was not supremely confident that their marks were correct - especially when they know that the marks were wrong).

Put another way, there is an ongoing tension between accuracy and independence when considering hard to value securities.

Three Thoughts Around Valuation

There are many points to raise in the valuation debate: however, we'd like to highlight three. These issues are, in our mind, foundational to the valuation process - but are equally uncomfortable as they challenge current "orthodoxy" around hedge fund pricing procedures.

To our final point, we opened a random PPM on our desk this morning and found the following disclaimer around administration responsibility. For investors, take a moment and read this language - this is the standard of care the administration industry has now slid back to, notwithstanding that administration fees are paid for by investors. What exactly are we paying for?

For the purpose of calculating the Partnership’s net asset value, the Administrator relies on, and shall be entitled to rely on, and will not be responsible for the accuracy of financial data furnished to it by the Investment Adviser, the Partnership’s custodians and prime brokers, market makers and/or independent third party pricing services. The Administrator also may use and rely on industry standard financial models or other financials models approved by the General Partner or Investment Adviser in pricing the Partnership’s Securities or other assets. If and to the extent that the General Partner or the Investment Adviser is responsible for or otherwise involved in the pricing of any of the Partnership’s Securities or other assets, the Administrator may accept, use and rely on such prices in determining the Partnership’s net asset value and will not be liable to the Partnership in so doing.

When dealing with hard to value securities (and, let's face it, there's more hard to value than long / short equity in 2018), the administration service gap is, in our view, one of the most understated issues in the hedge fund industry. There is no easy answer, but we certainly encourage more discussion - before investors and administrators learn the implications....the hard way.