.png?width=200&height=78&name=CH%20Diligence%20(thicker%20line).png "Castle Hall Diligence - Logo.png")

.jpg)

Have the Big 4 crossed the line - are they now consultants doing auditing, not auditors who also consult? (And.....should they consult at all?)

I started my career as a trainee chartered accountant - not realizing exactly how hard the three years of exams in front of me would be - with Touche Ross. For those interested in the history of accounting mergers, in the UK Deloitte refused to merge with Touche - and for a couple of years a firm called "Coopers and Lybrand Deloitte" operated in the UK. Having said that, I then joined Price Waterhouse - and left a week before the merger with Coopers (that still remains a great piece of career timing!)

My best childhood friend - and subsequently the best man at my wedding - started his career, barely half a mile away, at Arthur Anderson. Little did we know that, 12 years later, Anderson would implode over the Enron fiasco.

It is now more than 15 years since the failure of Anderson...which seems as if it may have been more than enough time for some of the old bad habits to creep back into the accounting "profession".

In the US, the national managing partner in charge of audit quality and professional practice at KPMG has been charged with fraud by the SEC.

He's not the only one.

Also charged is the KPMG national managing partner in charge of audit quality inspections conducted by the PCAOB (Public Company Accounting Oversight Board). Also facing trial (and hopefully jail, if the allegations are proven in court) is the KPMG partner who was co-head of the firm's entire banking and capital markets practice.

What??????

In 2013, the PCAOB conducted a review of KPMG's audits, which, per the SEC complaint, found that of the 50 audits inspected, 23 - 46% - were deficient. This was bad news, as the prior year, only (!!!) 34% had been deficient.

The answer of the lead partner within KPMG's audit quality and oversight units? Hire someone from the PCAOB, who joined KPMG....conveniently bringing with him a USB thumb drive listing the audit clients which would be examined the following year.

These are not junior staffers. These are the MOST SENIOR professionals within the entire audit quality leadership group of a Big 4 audit firm. For the diligence practitioners reading this blog who are qualified accountants - we all know exactly what this means.

The one saving grace in this professionally repugnant story is that another KPMG audit partner contacted by "technical" asking to review (and re-open) the prior year audit working papers thought the specificity of the requests to be suspicious. Per the SEC, the technical group's requests "made her (the audit partner) suspect that the firm may have received confidential PCAOB information". This partner then reported her suspicions to KPMG's Office of General Counsel, which led to KPMG self-reporting the events to the SEC.

Looking more broadly, though, there is an unfortunate and likely unavoidable conclusion. While this sorry episode happened at KPMG, professionals of this seniority, tenure and professional credibility sit in all of the Big 4 firms. So, it's not unreasonable to assume that this could just have easily have happened to Deloitte, EY or PwC. And at large law firms and other professional service providers who provide services to investment funds, supposedly providing "gatekeeper" protections for investors.

Meanwhile, in the UK, there have been some very high profile audit failures, notably British Home Stores (BHS), where PwC have just been fined 10 million pounds, partly because the audit partner conveniently backdated his audit opinion during a sale process...recording the grand total of two hours of chargeable time during his review process. The company subsequently collapsed, resulting in the biggest pension fund scandal the UK has ever seen (at least since Robert Maxwell!)

Other failures in the UK include Carillion, a construction company which imploded earlier this year (auditor - KPMG). In South Africa, Steinhoff appears to be another example where the GAAS audit process completely failed to identify a wholesale fraud (auditor - Deloitte). And don't get us started on Sino Forest (EY - who paid $8million - without admitting or denying liability to the Ontario, Canada securities regulator).

After quickly picking four examples which "implicate" each member of the Big Four - where do we go from here?

Per the FT, the UK watchdog with responsibility for the accounting profession, the Financial Conduct Authority, is now calling for a split of the Big 4.

"Stephen Haddrill, chief executive of the Financial Reporting Council that regulates accountants, said Britain's Competition and Markets Auditory should investigate the case for "audit only" firms in an effort to bolster competition and stamp out conflicts of interest".

(In separate news, the fifth largest audit firm in the UK, Grant Thornton, has announced that they will no longer bid on audits on any of the FTSE 350 - the largest 350 companies in the UK stock market. In Britain, this leaves the audit market entirely captive to the Big 4.)

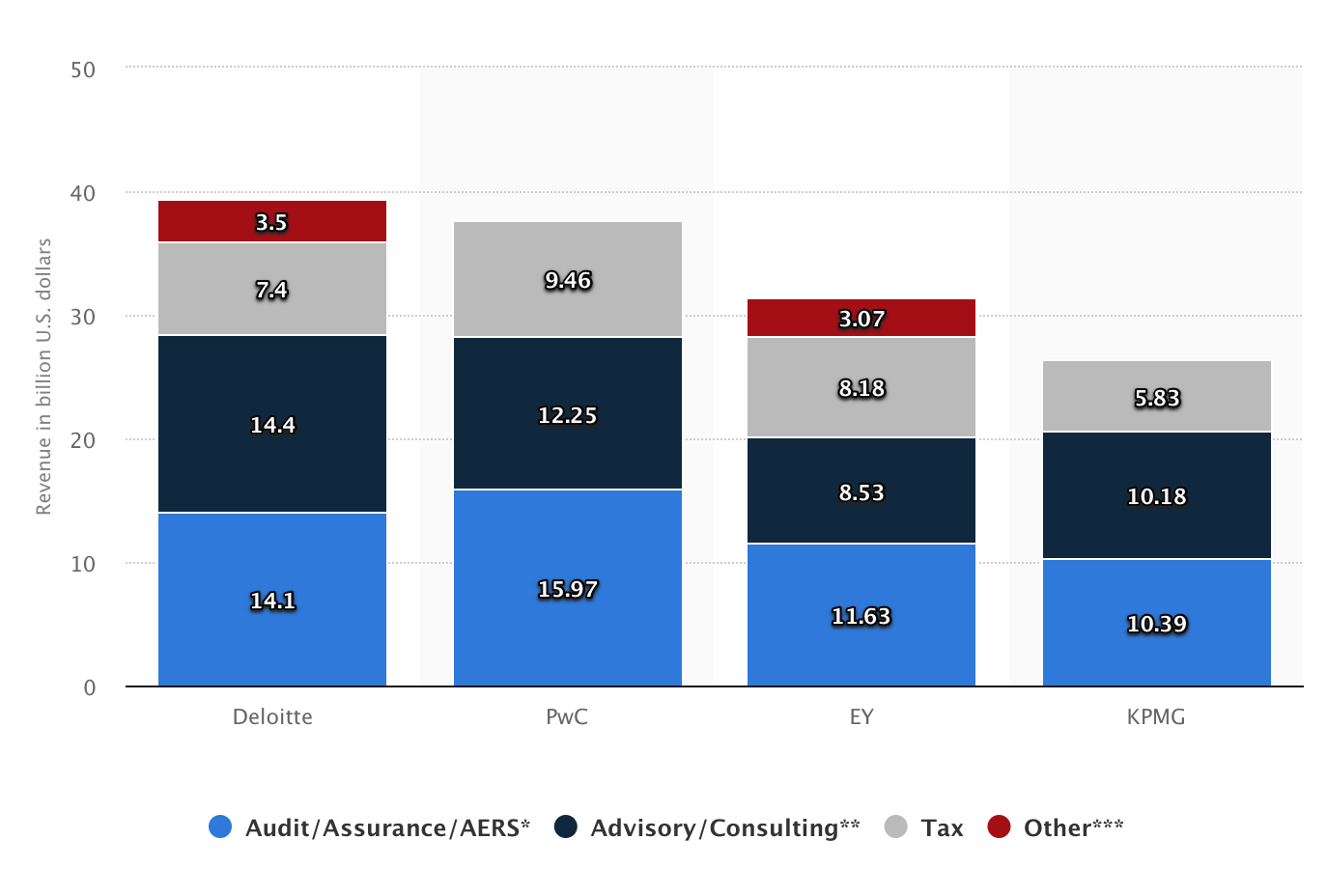

The heart of the issue is the revenue generated by different business lines. This chart shows the percentages of revenue generated worldwide by the Big 4 in different service lines.

For the Big 4, according to this source, the percentage of income generated from audit services was:

Deloitte: 36%

PwC: 42%

EY: 37%

KPMG: 39%

Let's face facts: the moment that audit becomes a minority of revenue, an audit firm is not an audit firm - they are a consulting firm that also completes audits. And, to put the timing and sequence of these changes in context - per the WSJ, since 2012, Big 4 income from consulting and advisory has risen 44% - whilst boring old audit is only up 3%. This reversal from the Big 4 being audit firms, to becoming consulting firms, has happened over the past 5 years.

From the perspective of investors conducting due diligence on their third party asset managers, what does this mean?

Interesting times ahead.